16 June 2026

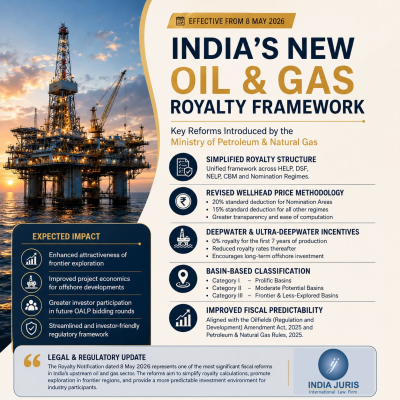

On 8 May 2026, the Ministry of Petroleum and Natural Gas issued a gazette notification amending the Schedule to the Oilfields (Regulation and Development) Act, 1948 (“ORD Act”), overhauling the royalty structure for crude oil, casing head condensate, and natural gas production across all exploration and production regimes.

I. BACKGROUND AND LEGISLATIVE BASIS

Royalties on mineral oil production in India are levied under the authority of Section 6A of the Oilfields (Regulation and Development) Act, 1948 (the “ORD Act”). The provision empowers the Central Government to determine the rate of royalty payable in respect of any mineral oil won from a leased area and to amend the Schedule setting out those rates.

The royalty framework had historically accreted through successive policy layers, nomination-based awards to national oil companies, the pre-NELP contractual regime, the New Exploration Licensing Policy (“NELP”), the Hydrocarbon Exploration and Licensing Policy (“HELP”) introduced in 2016, the Discovered Small Field Policy (“DSF Policy”), and the Coal Bed Methane (“CBM”) Policy, each carrying its own royalty obligations. The resulting multiplicity of rate structures created inconsistencies and administrative complexity that the government has long sought to rationalise.

The immediate legal trigger for the present reform is the Oilfields (Regulation and Development) Amendment Act, 2025 (the “ORD Amendment Act”), and the Petroleum and Natural Gas Rules, 2025 (the “PNGR 2025”). Both instruments overhauled the operational framework for upstream exploration and production, and the revised royalty schedule is expressly described by the government as “decade-long effort” and “the culmination” of those 2025 reforms.

II. The Gazette Notification of 8 May 2026

The Ministry of Petroleum and Natural Gas published a gazette notification dated 8 May 2026 (the “Royalty Notification”), amending the Schedule appended to Section 6A(4) of the ORD Act. The Royalty Notification replaces the existing Schedule in its entirety and introduces a restructured rate framework applicable across all categories of exploration and production areas.

A. Revised Rate Structure

The notification introduces differentiated royalty rates across the following principal categories:

Crude Oil / Condensate

Natural Gas

Special Provision

Onland

Shallow Water

Deepwater

Ultra-Deepwater

Projects commencing production within:

will be eligible for the following concessional royalty rates:

B. Revised Wellhead Price Methodology

A significant operational change introduced by the Royalty Notification concerns the method of computing the “wellhead price,” which forms the basis for royalty calculation. Under the prior regime, royalty was assessed on a price derived by deducting actual post-wellhead costs, transportation, processing, and handling, from the gross sale price. The resulting methodology often involved case-specific determination of post-wellhead costs, leading to administrative complexity and valuation issues.

The Royalty Notification replaces actual-cost deductions with a standardised flat deduction:

The notification further provides that royalty shall be computed on an ex-royalty basis across all regimes. Taken together, these changes are expected to reduce the effective royalty burden and simplify royalty computation.

III. Sedimentary Basin Classification

The Royalty Notification introduces a statutory three-tier classification of India’s sedimentary basins. The classification determines the concessional rate applicable to HELP contracts where commercial production commences within the prescribed timeline.

The basin classification is consequential for operators competing in OALP Rounds X and XI, as the lower royalty rates applicable to Category III basins may improve the commercial attractiveness of frontier exploration.

IV. LEGAL AND REGULATORY ANALYSIS

A. Relationship with the ORD Amendment Act, 2025 and PNGR 2025

The Royalty Notification sits within a broader legislative architecture. The ORD Amendment Act, 2025 expanded the definition of “mineral oils” to include unconventional hydrocarbons, replaced the “mining lease” with the “petroleum lease” as the operative instrument, and conferred statutory authority to frame rules on infrastructure sharing, dispute resolution, and conferred statutory authority to frame rules on infrastructure sharing, dispute resolution, safety and other operational matters. The PNGR 2025, in turn, replaced the sixty-six-year-old Petroleum and Natural Gas Rules, 1959 with a comprehensive 65-rule framework providing for a unified petroleum lease, stabilisation protections and enhanced operational and environmental safeguards.

The Royalty Notification is the third pillar of this reform cycle: where the ORD Amendment Act provided the statutory authority and the PNGR 2025 reorganised the operational framework, the Royalty Notification now rationalises the fiscal terms. Taken together, the three instruments are intended to present a coherent, investor-aligned upstream regulatory package

B. Stabilisation and Fiscal Predictability

An important interaction exists between the Royalty Notification and the stabilisation clause introduced by the PNGR 2025. The PNGR 2025 provides a mechanism by which lessees may claim compensation for adverse changes in law that materially affect the commercial viability of a project, including increases in taxes, royalties, or levies. The Royalty Notification, being a downward revision of royalty rates, would not ordinarily engage this mechanism. However, future increases in royalty rates may, depending on the circumstances and the terms of the applicable petroleum lease, attract the operation of the stabilisation provisions.

C. Treatment of Pre-Existing Contracts

The Royalty Notification applies across both legacy and future production regimes, including nomination areas, pre-NELP contracts, NELP blocks, CBM areas, DSF contracts and HELP blocks. For operators under pre-NELP and NELP production sharing contracts, the revised schedule largely preserves the existing royalty structure while simplifying the methodology for royalty computation. As the notification generally reduces or maintains the royalty burden, it is unlikely to give rise to the kinds of adverse change-in-law issues that can accompany upward fiscal revisions.

D. Ultra-Deepwater and Frontier Investment Incentive

The introduction of a nil royalty for the first seven years of commercial production from ultra-deepwater blocks, followed by substantially reduced royalty rates thereafter, represents a significant departure from earlier fiscal terms. ICRA has observed that the revised framework could meaningfully improve the economics of upstream exploration investments, particularly for offshore projects where capital costs are high and development timelines are long. CLSA has estimated that the royalty rationalisation could increase ONGC’s fair value by 7–9% and Oil India’s by 9–11%, although the benefits of the revised regime for new offshore developments are likely to be realised only over the medium term.

V. CONCLUDING OBSERVATIONS

The revised royalty framework notified on 8 May 2026 represents one of the most significant recent fiscal reforms in India’s upstream oil and gas sector. Its importance lies not merely in the reduction of royalty rates, but also in three structural features: the adoption of a standardised wellhead price deduction formula that simplifies royalty computation; the introduction of a basin-based classification that aligns royalty incentives with geological risk; and its integration into the broader statutory framework established by the ORD Amendment Act, 2025 and the Petroleum and Natural Gas Rules, 2025.

The ultimate measure of the reform’s success will be whether it translates into greater investor participation in future OALP bidding rounds. The repeated extensions of bidding timelines suggest that legislative reform alone may not be sufficient; investor confidence will ultimately depend on the Government’s ability to administer the revised framework in a manner that delivers the certainty and predictability that the reforms are intended to achieve.